The Political Animal and the Office Market

A framework for interpreting global office demand in 2026

Aristotle described the human being as a political animal. The observation has not lost relevance. With work comes hierarchies, influence, missing information and decisions. Weber’s analysis of bureaucracy carried the idea further: large organisations require predictable settings where authority can be expressed, observed and transferred.

These conditions still shape office markets in 2026.

Hybrid work changes utilisation patterns, but it has not removed the political mechanics of organisational life. Many firms still rely on physical proximity through which ideas are accepted or rejected.

For investors, the anchor question is therefore not “will the office come back?” but “where does the organisation of authority still rely on being in the room?”

A Framework for Reading Office Markets

Office demand is structurally resilient where three conditions hold:

1. Institutional Core Intensity

Whether a city has a clear centre where major decisions are made — typically government, big banks, large law firms and regulators concentrated in one area.

2. Corporate Depth

Whether firms have real hierarchies where careers depend on being seen, building internal relationships and working around senior staff.

3. Sectoral Need for Co-Presence

Whether the city’s main industries work better in person — for example, finance, law, consulting and public administration — rather than industries that can operate easily at distance, like tech.

When these conditions are present, office use is anchored and generally creates its own demand. Otherwise, demand may be fickle.

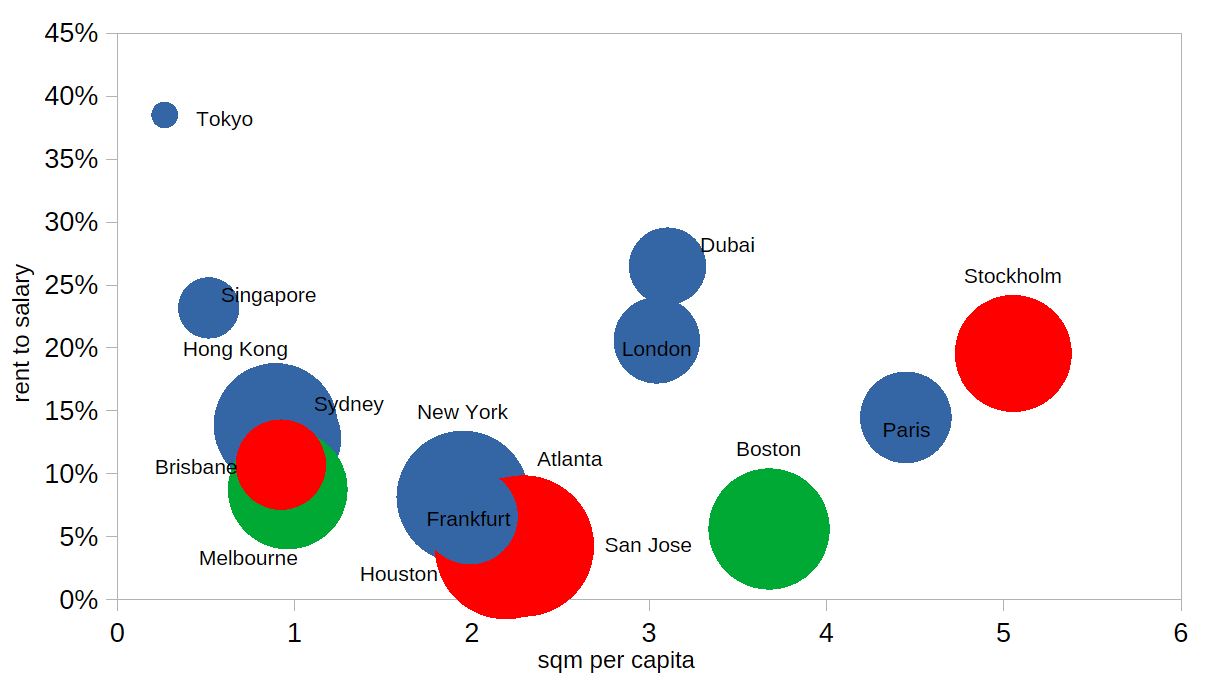

The chart below plots three simple indicators that reflect these criteria in practice:

Rent burden on the vertical axis (cost of 10 sqm as a share of average salary, local dollars),

Office stock per capita (square metres) on the horizontal axis and

Vacancy rate shown by bubble size.

These measures capture how strongly a city relies on co-present decision-making and how well its office market is aligned with its economic structure. The position of each city on the chart reflects the strength or weakness of its institutional core, corporate depth and sectoral need for presence.

Category 1: Institutional Command Centres

(High rent burden; mid-to-high office stock per capita; low-to-moderate vacancy)

These cities contain established decision-making precincts with deep corporate hierarchies. Demand for top-tier offices persists even as utilisation patterns change. Grade A assets remain core infrastructure; secondary stock absorbs the shift.

New York

Decision-making remains centred on Midtown, Midtown East and Lower Manhattan. Senior coordination is in-person. Vacancy in secondary stock reflects obsolescence, not a collapse in the function of the core.

Sydney

Sydney’s CBD serves as Australia’s institutional centre for finance, law and advisory work. Organisational depth is high and presence expectations remain embedded. Patterns mirror New York: strong core, weak periphery.

London

The City and the West End form a two-node institutional geography. Key sectors still coordinate through face-to-face routines. Vacancy concentrates in assets without institutional relevance.

Paris

A dual core - the administrative centre and La Défense - concentrates authority for major corporates and public institutions. These sectors maintain hierarchical, presence-based decision structures.

Frankfurt

Decision-making is concentrated in the Bankenviertel and associated regulatory precincts. The market is narrow but institutionally anchored.

Singapore

Marina Bay and Raffles Place serve as the region’s central hubs for finance and regulatory-adjacent work. Coordination remains spatially concentrated.

Hong Kong

Central and Admiralty continue to host the city’s significant financial and legal institutions. Vacancy remains manageable in the relevant submarkets.

Tokyo

Marunouchi and Otemachi house major corporate groups. Decision-making relies on established organisational forms that function best in person.

Dubai

DIFC, Business Bay and adjacent precincts operate as regional coordination hubs. Although corporate structures can be more mobile than in older markets, decision-making for key sectors is increasingly anchored in these districts.

Investment implication: These cities retain a structural requirement for high-quality office space. Core assets preserve liquidity and pricing power; B-grade assets face prolonged repositioning or exit.

Category 2: Selective Institutional Anchors

(Moderate rent burden; moderate stock; mixed vacancy)

Unlike command centres, these cities have identifiable pockets of institutional depth, but authority is not as tightly concentrated. Demand is strong only where the local economy has a clear coordination centre.

Boston

Research, healthcare and specialised finance form a cluster with strong presence expectations. Outside these nodes, office utilisation is flexible — meaning vacancy can bite.

Melbourne

Like its physical geography, Melbourne’s corporate structure is flatter, with authority distributed across sectors and campuses. The CBD functions, but does not anchor national decision-making in the same way Sydney does.

Atlanta

Atlanta has several active business districts, but authority is spread across firms rather than concentrated in a core. Office demand bifurcates accordingly.

Investment implication: Selective exposure works. Prime assets in institutional nodes perform; the broader market offers weak structural support.

Category 3: Weak Structural Anchors

(Low rent burden; high vacancy; misalignment between stock and institutional structure)

Dominant industries in these cities do not rely on deep hierarchies or co-located decision-making. Authority is either distributed, mobile or external to the CBD.

Silicon Valley/San Jose

Technology’s governance model is project-based and executive-portable. Internal coordination occurs across distributed teams. The centre has no binding institutional purpose.

Stockholm

A digital economy with flatter organisational structures and high acceptance of remote modes. Older office districts exceed current institutional requirements.

Houston

Energy firms concentrate authority within executive groups but not within the CBD. Corporate campuses substitute for traditional office towers.

Brisbane

Brisbane’s CBD is effective but not a national or regional command centre. Authority does not gravitate to a single precinct.

Investment implication: Office assets behave more like discretionary overhead than organisational infrastructure. Vacancy is a structural condition, not a temporary cycle.

Conclusion

The message for investors is straightforward. Offices hold their value where decisions still get made in person. Cities with strong institutional cores will keep absorbing good space. Cities without them won’t. It is not about office “coming back” — it’s really about where authority needs to be. That’s also where capital will sit.